Reinforcement Learning in kdb+/q: Q-learning

Reinforcement Learning is an area of machine learning that studies how autonomous agents learn to behave by taking actions and receiving rewards.

We present an approach for training an agent to behave optimally in a trading environment. We model such an environment with some simplifying assumptions:

- There is only one opportunity to trade per day which must be done by paying

the

closeprice provided in historical market data. - An agent either has a long or short position in one security. The exact number of shares is made irrelevant by using cumulative returns.

- No transaction costs are taken into account.

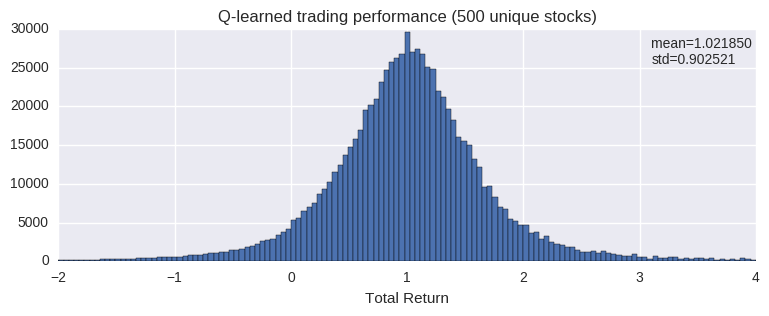

Using a simple set of technical indicators derived from market data an agent is trained using the Q-learning algorithm. Once trained, the agent’s knowledge is tested by performing out-of-sample trading. Market data from 500 stocks are used, spanning 10+ years.

Performance

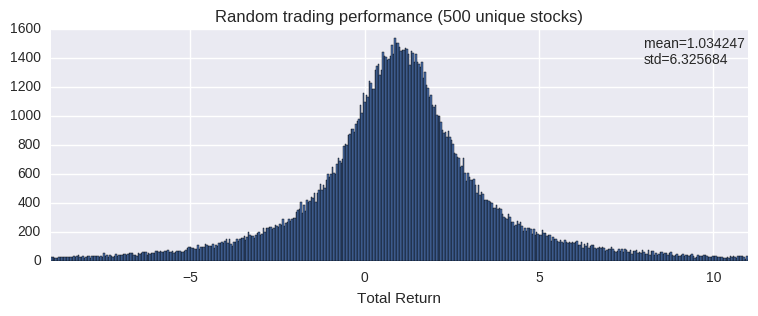

Initial results suggest lack luster average returns, but seemingly better than random trading, which produces similar average return with higher standard deviation. A return of 1.0 means the agent has as much money at the end of trading as it did at the start.

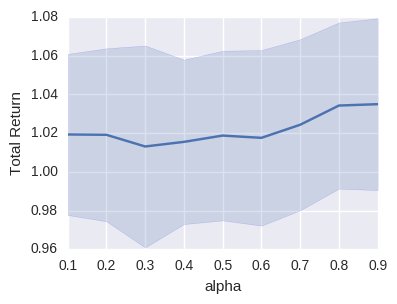

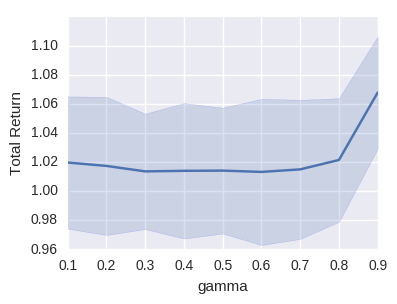

alpha & gamma

In the Q-learning algorithm alpha and gamma control the learning and discount rates, respectively. Our results show a marginal improvement in returns when training with higher alpha and gamma values.

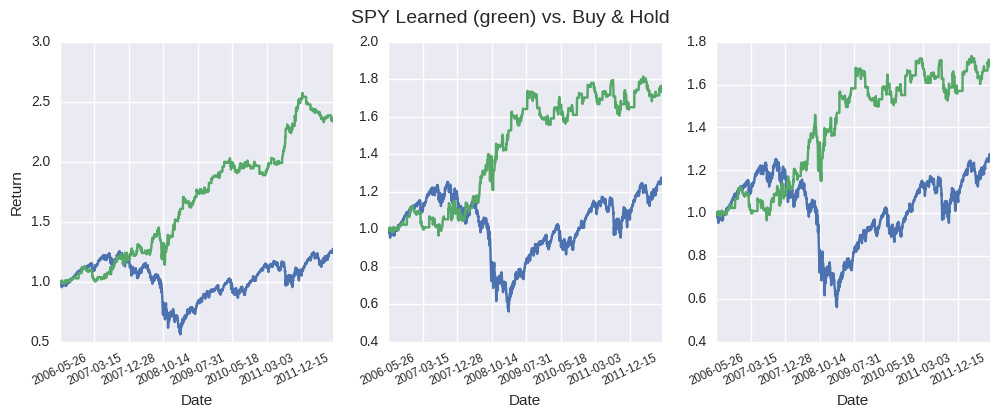

Trading SPY

Here we present the best learned trading strategies from a batch of 100 trainings.

Link to code: github.com/jlas/ml.q/tree/master/rl/experiment/trade